Probability TableThe script is inspired by user NickbarComb, I suggested checking out his Price Convergence script.

Basically, this script plots a table containing the probability of the current candle closing either higher or lower based on user-define past period.

Hope that it will be helpful.

Pesquisar nos scripts por " TABLE "

TFi Price Action Resampling Filter V1 - FULLThe script is resampling the price based on its range/price-action and creates an alternative filter to smoothen price movements.

Overview of features:

Optional stop-loss

Optional flags to control the position entry

Optional flags to control the position exit

Built-in backtesting engine with start balance, position size and pyramiding; each year will be evaluated separately

Inputs for a percentage entry and exit slippage, entry/exit and daily funding fees

Configurable alerts, which follow the exact position of the entry/exit marker

Alert messages contain predefined trading instruction to execute orders via Alertatron or TradeFab's proprietary trading server, or can be defined by the user

The script renders a performance/status table, which shows the current position status and result of the built-in trading simulation results.

It shows the following statistic values:

Current position PnL - also background turns green if position is in profit and red if in loss

Average entry price and number of positions

Current percentage distance to the optional stop-loss level

Current Maximum Draw Down

Number of wins and losses and the win/loss ratio per year and overall

Profit and loss amount, paid fees per year and overall

Profit-ratio and Maximum Draw Down per year and overall

Balance and ROI per year and overall

MTF Price/Volume % [Anan]Hello friends,

This is a multi-timeframe table with these features:

Display price change percentage compared with the last timeframe candle close.

Display price change percentage compared with the last timeframe candle close MA.

Displays change percentage compared with the last timeframe candle volume.

Displays change percentage compared with the last timeframe candle volume MA.

Change type/length of MA for Price/Volume.

Full control of Panel position and size.

Full control of displaying any row or column.

Average Daily Range TableThis is the last script to complete Vladimir Poltoratskiy's setup found in his books.

Poltoratskiy argues that you should not take any fractal corridors higher than 50% of the Average Daily Range. To be honest, even 40% is a lot, because then, your target will be 160% ADR away from your entry and one "fracture" just can't be enough to predict moves this big.

I chose a table to visually represent the indicator because it doesn't change its value during the day. It takes far less room on the chart.

There are also two simple moving averages. You may use the as an indicator if the relative volatility as of late is extremely low and in that case, perhaps, expect an increase in the coming days. They are applied to the Average Daily Range, not one day range!

Relative Volume TableRelative Volume Table in percent. So 400% RVol means, today's volume is 4x compared to avg volume for the length you selected.

1. When chart resolution is Daily or Intraday (D, 4H, 1H, 5min, etc), Relative Volume shows value based on DAILY.

2. When resolution is changed to Weekly or Monthly, then Relative Volume shows corresponding value. i.e. Weekly shows weekly relative volume of this week compared to past 'N' weeks. Likewise for Monthly. You would see change in label name. Like, Weekly chart shows W_RVol (Weekly Relative Volume). Likewise, Daily & Intraday shows D_RVol. Monthly shows M_RVol (Monthly Relative Volume).

3. Added a plot (by default hidden) for this specific reason: When you move the cursor to focus specific candle, then Indicator Value displays relative volume of that specific candle. This applies to Intraday as well. So if you're in 1HR chart and move the cursor to a specific candle, Indicator Value shows relative volume for that specific candlestick bar.

Hope you find this useful.

PAC newThis indicator will alert you when a candle goes above or below the price action channel (PAC) but only on the first or second candle after a colour change in candle.

When price is above the price action channel that is a bullish sign, when price is below the PAC that is a bearish sign.

The idea is that a sudden change in price is a cause to investigate further price action moving in that direction so the indicator aims to identify reversal

Scalping strategy that works on 5 min chart and aims to gain 10 pips. Do not act on every signal. Further investigation is required, for example by looking at RSI oversolf and overbought levels. For example, at an oversold area, a buy signal is more valid

Table: Forex Central Bank Interest RatesThis tool shows CB Interest Rates for USD, JPY, CAD, CHF, EUR, GBP, NZD, AUD - basically all the majors.

Use override and input your own value if it is changed and I haven't updated the script yet.

Month/Month Percentage % Change, Historical; Seasonal TendencyTable of monthly % changes in Average Price over the last 10 years (or the 10 yrs prior to input year).

Useful for gauging seasonal tendencies of an asset; backtesting monthly volatility and bullish/bearish tendency.

~~User Inputs~~

Choose measure of average: sma(close), sma(ohlc4), vwap(close), vwma(close).

Show last 10yrs, with 10yr average % change, or to just show single year.

Chose input year; with the indicator auto calculating the prior 10 years.

Choose color for labels and size for labels; choose +Ve value color and -Ve value color.

Set 'Daily bars in month': 21 for Forex/Commodities/Indices; 30 for Crypto.

Set precision: decimal places

~~notes~~

-designed for use on Daily timeframe (tradingview is buggy on monthly timeframe calculations, and less precise on weekly timeframe calculations).

-where Current month of year has not occurred yet, will print 9yr average.

-calculates the average change of displayed month compared to the previous month: i.e. Jan22 value represents whole of Jan22 compared to whole of Dec21.

-table displays on the chart over the input year; so for ES, with 2010 selected; shows values from 2001-2010, displaying across 2010-2011 on the chart.

-plots on seperate right hand side scale, so can be shrunk and dragged vertically.

-thanks to @gabx11 for the suggestion which inspired me to write this

Koalafied Risk ManagementTables and labels/lines showing trade levels and risk/reward. Use to manage trade risk compared to portfolio size.

Initial design optimised for tickers denominated against USD.

Multi-Session High/Low Trackertable that shows rth eth and full weekly range high and low with range difference from high and low

Table ATH and DayQuotes in the middle of a chartJust important things at a glance ..

AlltimeHigh and Daily High/Low

Argentum Flag [AGP]Ver.2.1Technical Description of the "Argentum Flag " Indicator

The "Argentum Flag " is a multifaceted trading indicator designed to provide a comprehensive view of market dynamics by combining elements of trend, volatility, momentum, and volume analysis. Its architecture is built on the synergy of multiple technical tools, allowing traders to make more informed decisions by reducing market noise and focusing on high-probability inflection points.

1. Dynamic AGP Bands (EMA 36 and Percentage Levels)

The core of the indicator is a 36-period Exponential Moving Average (EMA), which acts as the price's baseline and center of gravity. From this EMA, the script plots dynamic bands at predefined percentages (Base, Prime, and Vortex).

Logic: These bands are not static like Bollinger Bands; they expand and contract in response to the underlying EMA. This methodology helps identify relative volatility and trend strength. When the price trades within these bands, it's considered to be in a range or a controlled consolidation.

Benefit to the Trader: They provide a quick visual of dynamic support and resistance levels. A price movement beyond the Vortex band can signal an extreme market imbalance, suggesting potential trend exhaustion or a high-energy breakout.

2. Breakout Signals (Signals)

The indicator generates plotshape signals when the price stays outside the volatility bands for a specific number of consecutive bars (2 for the Prime band and 3 for the Vortex band).

Logic: These signals act as an overextension detection system. The underlying principle is that once the price breaks and holds outside these zones, the probability of a pullback or a reversal increases significantly. The lastSignalBarIndex logic prevents signal overload and ensures a cooling-off period, eliminating noise from consecutive signals.

Benefit to the Trader: It provides clear visual alerts for taking profits or looking for potential reversals. A trader can use the Vortex band exit signal (⌾) as confirmation to close a long or short position, while the Prime band signal (⍲) can indicate a potential pullback for a trend-following entry.

3. Bar Volume Analysis (Barcolor)

The script introduces a sophisticated bar coloring system that classifies volume activity relative to a 50-period Simple Moving Average (SMA).

Logic: The coloring is based not only on whether the bar is bullish or bearish but also on the magnitude of the volume. For instance, extreme volume (more than 3.5 times the average volume) is colored blue, indicating institutional participation or a high-impact event. High (1.8x) or average (0.6x - 1.7x) volume is distinguished with other colors, providing a visual map of the underlying strength behind each price move.

Benefit to the Trader: It allows for a quick identification of bars with the highest market conviction. A bearish price bar with extreme volume (extreme_volume_bearish) might signal significant liquidation, while a bullish bar with extreme volume (extreme_volume_bullish) could suggest strong accumulation.

4. Real-Time Monitoring Tables (EMA and RSI)

The indicator includes two data tables in the bottom corner of the screen, acting as a dashboard for multi-timeframe analysis.

EMA Table (Fibonacci): This table shows the current values of a series of Fibonacci-based EMAs (13, 21, 34, etc.). The background color of each cell indicates whether the current price is above (white) or below (blue) the corresponding EMA.

Logic: This table allows traders to assess the trend bias across different timeframes, from short to long-term. An alignment of multiple EMAs in the same direction (e.g., all white) confirms a strong trend.

Benefit to the Trader: It provides a quick check for trend confirmation. For example, before opening a long position on a 5-minute chart, a trader can verify if the overall trend on higher timeframes (e.g., 4h or 1D) is also bullish.

RSI Table (Multi-Timeframe): This table shows the Relative Strength Index (RSI) values across multiple timeframes, from 1 minute to monthly. The cell lights up orange if the RSI is in the overbought zone (> 77) or white if it's in the oversold zone (< 23).

Logic: The use of request.security enables the fetching of data from other timeframes on the current bar. This is a crucial component for multi-timeframe divergence analysis.

Benefit to the Trader: It helps identify overbought or oversold conditions across different trading horizons, which is vital for spotting large-scale reversals. If the 1D and 4h RSIs are overbought, a long position on a lower timeframe could be high-risk.

Competitive Advantages for Traders

The "Argentum Flag " is not just a simple indicator; it's a consolidated technical analysis suite that saves time and effort. Instead of overlaying multiple indicators, a trader gets all the relevant information in a single view. The contextualized volume analysis and volatility-based signals are invaluable tools for filtering out low-quality entries and exits. Finally, the real-time monitoring tables provide a multi-timeframe perspective that is fundamental for validating market direction and managing risk.

In trading, the convergence of multiple technical data points is key to increasing the probability of success. This indicator provides precisely that convergence, enabling both novice and experienced traders to make more precise and strategic decisions.

Risk Warning (Disclaimer)

Trading in financial markets carries a significant risk of loss and is not suitable for all investors. The information and signals provided by this indicator are for educational and analysis purposes only and should not be construed as financial advice. The past performance of any trading system or methodology is not necessarily indicative of future results. The user assumes all responsibility for their own trading decisions and any resulting losses or gains.

Auto-Anchored MA with Deviation BandsAuto-Anchored MA with Deviation Bands

✨ Features

📈 Auto-Anchored MA: Calculates moving averages (EMA, SMA, EWMA, WMA, VWAP, TEMA) anchored to user-defined periods (Hour, Day, Week, etc.).📏 Deviation Bands: Plots upper/lower bands using Percentage or Standard Deviation modes for volatility analysis.⚙️ Customizable Timeframes: Choose anchor periods from Hour to Year for flexible trend analysis.🎨 Visuals: Displays MA and bands with gradient fills, customizable colors, and adjustable display bars.⏱️ Countdown Table: Shows bars since the last anchor for easy tracking.🛠️ Smoothing: Applies smoothing to bands for cleaner visuals.

🛠️ How to Use

Add to Chart: Apply the indicator on TradingView.

Configure Inputs:

Anchor Settings: Select anchor period (e.g., Day, Week).

MA Settings: Choose MA type (e.g., VWAP, TEMA).

Deviation Settings: Set deviation mode (Percentage/Std Dev) and multipliers.

Display Settings: Adjust bars to display, colors, and gradient fill.

Analyze: View MA, deviation bands, and countdown table on the chart.

Track Trends: Use bands as dynamic support/resistance and monitor anchor resets.

🎯 Why Use It?

Dynamic Analysis: Auto-anchors MA to key timeframes for adaptive trend tracking.

Volatility Insight: Deviation bands highlight potential breakouts or reversals.

Customizable: Tailor MA type, timeframe, and visuals to your trading style.

User-Friendly: Clear visuals and countdown table simplify analysis.

📝 Notes

Ensure sufficient bars for accurate MA and deviation calculations.

Gradient fill enhances readability but can be disabled for simplicity.

Best used with complementary indicators like RSI or Bollinger Bands for robust strategies.

Happy trading! 🚀📈

Price Change % by rajib127Price Change % by rajib127

🎯 Key Features:

• Real-Time Multi-Timeframe Analysis - Track price changes across 15 different time periods (1 minute to 3 hours)

• Smart Color Coding - Green (profit), Red (loss), White (neutral) for instant visual recognition

• Highly Customizable Display - Toggle any timeframe on/off, adjust table position, size, and colors

• Universal Compatibility - Works on any chart timeframe without recalculation issues

• Clean Table Interface - Professional-looking data table that doesn't clutter your chart

📊 Supported Timeframes:

• Short-term: 1min, 2min, 3min, 4min, 5min, 10min

• Medium-term: 15min, 20min, 25min, 30min, 40min, 50min

• Long-term: 1 hour, 2 hours, 3 hours

⚙️ Customization Options:

• Individual Control - Enable/disable each timeframe independently

• Flexible Positioning - 9 different table positions (top, middle, bottom × left, center, right)

• Size Adjustment - 4 text size options (tiny, small, normal, large)

• Color Themes - Customizable background and text colors

💡 Perfect For:

• Day Traders - Quick percentage overview for scalping decisions

• Swing Traders - Monitor momentum across multiple timeframes

• Risk Management - Instant view of price volatility patterns

• Market Analysis - Compare short vs long-term price movements

🔧 Technical Advantages:

• 1-Minute Data Precision - Uses direct 1-minute data for accurate calculations

• No Lag Issues - Real-time updates without historical data delays

• Memory Efficient - Lightweight code that doesn't slow down your charts

• Error-Free Calculations - Handles all edge cases and data availability issues

📈 Use Cases:

• Monitor breakout strength across multiple timeframes

• Identify trending vs ranging market conditions

• Set alerts based on percentage thresholds

• Compare current volatility with recent periods

• Make informed entry/exit decisions

Installation: Simply add to chart and customize settings in the indicator panel. Works immediately on any symbol and timeframe!

Price Change % & Pips by rajib127📊 Multi-Timeframe Price Change Table — Pips & Percentage Tracker

This custom-built TradingView indicator provides a clean and detailed table showing pip and percentage changes across multiple timeframes. It helps traders quickly assess short-term and mid-term price momentum by visualizing how much the price has changed over different intervals.

🔍 Features:

Displays pip change and percentage change side-by-side.

Covers a wide range of timeframes:

• Minute-based: M01, M02, M03, M04, M05, M10, M15, M20, M25, M30, M40, M50

• Hour-based: H01, H02, H03

Color-coded values for quick visual interpretation:

• 🟢 Positive movement (price increase)

• 🔴 Negative movement (price decrease)

Ideal for scalpers, day traders, and short-term swing traders.

🎯 Use Case:

This tool is designed to help you:

Detect early momentum shifts

Spot short-term trends or reversals

Confirm trade entries or exits based on recent price behavior

🛠 Customizable:

The script can be further extended or customized to include different timeframes, alert conditions, or integrate with other strategies.

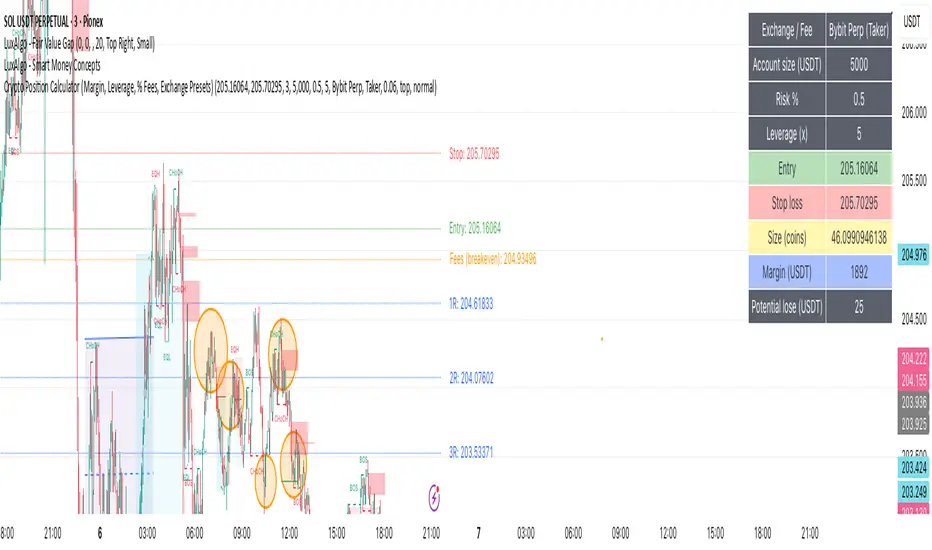

Crypto Position CalculatorAlpha2Million - Crypto Position Calculator (Margin, Leverage, % Fees, Exchange Presets)

This script is a crypto trading risk & position calculator built directly into TradingView.

It helps futures/perpetual traders size positions, calculate margin requirements, and visualize risk-to-reward levels on the chart — with exchange fee presets for real-world accuracy.

• Position Sizing by Risk %

• Enter account size and % risk per trade.

• Script calculates exact position size (coins) based on SL distance.

• Leverage & Margin

• Shows required notional and margin (USDT) for the trade.

• Exchange Fee Presets

• Supports Binance, Bybit, Pionex, MEXC, Gate.io, KuCoin, HTX.

• Maker vs Taker fee selection.

• Custom option to enter your own per-side fee %.

• Fee Breakeven Line (Orange)

• Plots the exact price level you need to reach to cover entry + exit fees.

• Lets you see how far price must move before you are at true breakeven.

• Risk vs Reward Calculation

• Risk is calculated on price movement only (SL distance).

• Profit targets include fees, so “1R / 2R / 3R (net)” lines show realistic levels.

• Smart Table Display

• Account size, leverage, entry, stop, target.

• Position size (coins), notional (USDT), required margin.

• Risk at SL, fees (round trip), fee breakeven move/price.

• Profit @ TP (after fees) and net RR.

Universal Ratio Trend Matrix [InvestorUnknown]The Universal Ratio Trend Matrix is designed for trend analysis on asset/asset ratios, supporting up to 40 different assets. Its primary purpose is to help identify which assets are outperforming others within a selection, providing a broad overview of market trends through a matrix of ratios. The indicator automatically expands the matrix based on the number of assets chosen, simplifying the process of comparing multiple assets in terms of performance.

Key features include the ability to choose from a narrow selection of indicators to perform the ratio trend analysis, allowing users to apply well-defined metrics to their comparison.

Drawback: Due to the computational intensity involved in calculating ratios across many assets, the indicator has a limitation related to loading speed. TradingView has time limits for calculations, and for users on the basic (free) plan, this could result in frequent errors due to exceeded time limits. To use the indicator effectively, users with any paid plans should run it on timeframes higher than 8h (the lowest timeframe on which it managed to load with 40 assets), as lower timeframes may not reliably load.

Indicators:

RSI_raw: Simple function to calculate the Relative Strength Index (RSI) of a source (asset price).

RSI_sma: Calculates RSI followed by a Simple Moving Average (SMA).

RSI_ema: Calculates RSI followed by an Exponential Moving Average (EMA).

CCI: Calculates the Commodity Channel Index (CCI).

Fisher: Implements the Fisher Transform to normalize prices.

Utility Functions:

f_remove_exchange_name: Strips the exchange name from asset tickers (e.g., "INDEX:BTCUSD" to "BTCUSD").

f_remove_exchange_name(simple string name) =>

string parts = str.split(name, ":")

string result = array.size(parts) > 1 ? array.get(parts, 1) : name

result

f_get_price: Retrieves the closing price of a given asset ticker using request.security().

f_constant_src: Checks if the source data is constant by comparing multiple consecutive values.

Inputs:

General settings allow users to select the number of tickers for analysis (used_assets) and choose the trend indicator (RSI, CCI, Fisher, etc.).

Table settings customize how trend scores are displayed in terms of text size, header visibility, highlighting options, and top-performing asset identification.

The script includes inputs for up to 40 assets, allowing the user to select various cryptocurrencies (e.g., BTCUSD, ETHUSD, SOLUSD) or other assets for trend analysis.

Price Arrays:

Price values for each asset are stored in variables (price_a1 to price_a40) initialized as na. These prices are updated only for the number of assets specified by the user (used_assets).

Trend scores for each asset are stored in separate arrays

// declare price variables as "na"

var float price_a1 = na, var float price_a2 = na, var float price_a3 = na, var float price_a4 = na, var float price_a5 = na

var float price_a6 = na, var float price_a7 = na, var float price_a8 = na, var float price_a9 = na, var float price_a10 = na

var float price_a11 = na, var float price_a12 = na, var float price_a13 = na, var float price_a14 = na, var float price_a15 = na

var float price_a16 = na, var float price_a17 = na, var float price_a18 = na, var float price_a19 = na, var float price_a20 = na

var float price_a21 = na, var float price_a22 = na, var float price_a23 = na, var float price_a24 = na, var float price_a25 = na

var float price_a26 = na, var float price_a27 = na, var float price_a28 = na, var float price_a29 = na, var float price_a30 = na

var float price_a31 = na, var float price_a32 = na, var float price_a33 = na, var float price_a34 = na, var float price_a35 = na

var float price_a36 = na, var float price_a37 = na, var float price_a38 = na, var float price_a39 = na, var float price_a40 = na

// create "empty" arrays to store trend scores

var a1_array = array.new_int(40, 0), var a2_array = array.new_int(40, 0), var a3_array = array.new_int(40, 0), var a4_array = array.new_int(40, 0)

var a5_array = array.new_int(40, 0), var a6_array = array.new_int(40, 0), var a7_array = array.new_int(40, 0), var a8_array = array.new_int(40, 0)

var a9_array = array.new_int(40, 0), var a10_array = array.new_int(40, 0), var a11_array = array.new_int(40, 0), var a12_array = array.new_int(40, 0)

var a13_array = array.new_int(40, 0), var a14_array = array.new_int(40, 0), var a15_array = array.new_int(40, 0), var a16_array = array.new_int(40, 0)

var a17_array = array.new_int(40, 0), var a18_array = array.new_int(40, 0), var a19_array = array.new_int(40, 0), var a20_array = array.new_int(40, 0)

var a21_array = array.new_int(40, 0), var a22_array = array.new_int(40, 0), var a23_array = array.new_int(40, 0), var a24_array = array.new_int(40, 0)

var a25_array = array.new_int(40, 0), var a26_array = array.new_int(40, 0), var a27_array = array.new_int(40, 0), var a28_array = array.new_int(40, 0)

var a29_array = array.new_int(40, 0), var a30_array = array.new_int(40, 0), var a31_array = array.new_int(40, 0), var a32_array = array.new_int(40, 0)

var a33_array = array.new_int(40, 0), var a34_array = array.new_int(40, 0), var a35_array = array.new_int(40, 0), var a36_array = array.new_int(40, 0)

var a37_array = array.new_int(40, 0), var a38_array = array.new_int(40, 0), var a39_array = array.new_int(40, 0), var a40_array = array.new_int(40, 0)

f_get_price(simple string ticker) =>

request.security(ticker, "", close)

// Prices for each USED asset

f_get_asset_price(asset_number, ticker) =>

if (used_assets >= asset_number)

f_get_price(ticker)

else

na

// overwrite empty variables with the prices if "used_assets" is greater or equal to the asset number

if barstate.isconfirmed // use barstate.isconfirmed to avoid "na prices" and calculation errors that result in empty cells in the table

price_a1 := f_get_asset_price(1, asset1), price_a2 := f_get_asset_price(2, asset2), price_a3 := f_get_asset_price(3, asset3), price_a4 := f_get_asset_price(4, asset4)

price_a5 := f_get_asset_price(5, asset5), price_a6 := f_get_asset_price(6, asset6), price_a7 := f_get_asset_price(7, asset7), price_a8 := f_get_asset_price(8, asset8)

price_a9 := f_get_asset_price(9, asset9), price_a10 := f_get_asset_price(10, asset10), price_a11 := f_get_asset_price(11, asset11), price_a12 := f_get_asset_price(12, asset12)

price_a13 := f_get_asset_price(13, asset13), price_a14 := f_get_asset_price(14, asset14), price_a15 := f_get_asset_price(15, asset15), price_a16 := f_get_asset_price(16, asset16)

price_a17 := f_get_asset_price(17, asset17), price_a18 := f_get_asset_price(18, asset18), price_a19 := f_get_asset_price(19, asset19), price_a20 := f_get_asset_price(20, asset20)

price_a21 := f_get_asset_price(21, asset21), price_a22 := f_get_asset_price(22, asset22), price_a23 := f_get_asset_price(23, asset23), price_a24 := f_get_asset_price(24, asset24)

price_a25 := f_get_asset_price(25, asset25), price_a26 := f_get_asset_price(26, asset26), price_a27 := f_get_asset_price(27, asset27), price_a28 := f_get_asset_price(28, asset28)

price_a29 := f_get_asset_price(29, asset29), price_a30 := f_get_asset_price(30, asset30), price_a31 := f_get_asset_price(31, asset31), price_a32 := f_get_asset_price(32, asset32)

price_a33 := f_get_asset_price(33, asset33), price_a34 := f_get_asset_price(34, asset34), price_a35 := f_get_asset_price(35, asset35), price_a36 := f_get_asset_price(36, asset36)

price_a37 := f_get_asset_price(37, asset37), price_a38 := f_get_asset_price(38, asset38), price_a39 := f_get_asset_price(39, asset39), price_a40 := f_get_asset_price(40, asset40)

Universal Indicator Calculation (f_calc_score):

This function allows switching between different trend indicators (RSI, CCI, Fisher) for flexibility.

It uses a switch-case structure to calculate the indicator score, where a positive trend is denoted by 1 and a negative trend by 0. Each indicator has its own logic to determine whether the asset is trending up or down.

// use switch to allow "universality" in indicator selection

f_calc_score(source, trend_indicator, int_1, int_2) =>

int score = na

if (not f_constant_src(source)) and source > 0.0 // Skip if you are using the same assets for ratio (for example BTC/BTC)

x = switch trend_indicator

"RSI (Raw)" => RSI_raw(source, int_1)

"RSI (SMA)" => RSI_sma(source, int_1, int_2)

"RSI (EMA)" => RSI_ema(source, int_1, int_2)

"CCI" => CCI(source, int_1)

"Fisher" => Fisher(source, int_1)

y = switch trend_indicator

"RSI (Raw)" => x > 50 ? 1 : 0

"RSI (SMA)" => x > 50 ? 1 : 0

"RSI (EMA)" => x > 50 ? 1 : 0

"CCI" => x > 0 ? 1 : 0

"Fisher" => x > x ? 1 : 0

score := y

else

score := 0

score

Array Setting Function (f_array_set):

This function populates an array with scores calculated for each asset based on a base price (p_base) divided by the prices of the individual assets.

It processes multiple assets (up to 40), calling the f_calc_score function for each.

// function to set values into the arrays

f_array_set(a_array, p_base) =>

array.set(a_array, 0, f_calc_score(p_base / price_a1, trend_indicator, int_1, int_2))

array.set(a_array, 1, f_calc_score(p_base / price_a2, trend_indicator, int_1, int_2))

array.set(a_array, 2, f_calc_score(p_base / price_a3, trend_indicator, int_1, int_2))

array.set(a_array, 3, f_calc_score(p_base / price_a4, trend_indicator, int_1, int_2))

array.set(a_array, 4, f_calc_score(p_base / price_a5, trend_indicator, int_1, int_2))

array.set(a_array, 5, f_calc_score(p_base / price_a6, trend_indicator, int_1, int_2))

array.set(a_array, 6, f_calc_score(p_base / price_a7, trend_indicator, int_1, int_2))

array.set(a_array, 7, f_calc_score(p_base / price_a8, trend_indicator, int_1, int_2))

array.set(a_array, 8, f_calc_score(p_base / price_a9, trend_indicator, int_1, int_2))

array.set(a_array, 9, f_calc_score(p_base / price_a10, trend_indicator, int_1, int_2))

array.set(a_array, 10, f_calc_score(p_base / price_a11, trend_indicator, int_1, int_2))

array.set(a_array, 11, f_calc_score(p_base / price_a12, trend_indicator, int_1, int_2))

array.set(a_array, 12, f_calc_score(p_base / price_a13, trend_indicator, int_1, int_2))

array.set(a_array, 13, f_calc_score(p_base / price_a14, trend_indicator, int_1, int_2))

array.set(a_array, 14, f_calc_score(p_base / price_a15, trend_indicator, int_1, int_2))

array.set(a_array, 15, f_calc_score(p_base / price_a16, trend_indicator, int_1, int_2))

array.set(a_array, 16, f_calc_score(p_base / price_a17, trend_indicator, int_1, int_2))

array.set(a_array, 17, f_calc_score(p_base / price_a18, trend_indicator, int_1, int_2))

array.set(a_array, 18, f_calc_score(p_base / price_a19, trend_indicator, int_1, int_2))

array.set(a_array, 19, f_calc_score(p_base / price_a20, trend_indicator, int_1, int_2))

array.set(a_array, 20, f_calc_score(p_base / price_a21, trend_indicator, int_1, int_2))

array.set(a_array, 21, f_calc_score(p_base / price_a22, trend_indicator, int_1, int_2))

array.set(a_array, 22, f_calc_score(p_base / price_a23, trend_indicator, int_1, int_2))

array.set(a_array, 23, f_calc_score(p_base / price_a24, trend_indicator, int_1, int_2))

array.set(a_array, 24, f_calc_score(p_base / price_a25, trend_indicator, int_1, int_2))

array.set(a_array, 25, f_calc_score(p_base / price_a26, trend_indicator, int_1, int_2))

array.set(a_array, 26, f_calc_score(p_base / price_a27, trend_indicator, int_1, int_2))

array.set(a_array, 27, f_calc_score(p_base / price_a28, trend_indicator, int_1, int_2))

array.set(a_array, 28, f_calc_score(p_base / price_a29, trend_indicator, int_1, int_2))

array.set(a_array, 29, f_calc_score(p_base / price_a30, trend_indicator, int_1, int_2))

array.set(a_array, 30, f_calc_score(p_base / price_a31, trend_indicator, int_1, int_2))

array.set(a_array, 31, f_calc_score(p_base / price_a32, trend_indicator, int_1, int_2))

array.set(a_array, 32, f_calc_score(p_base / price_a33, trend_indicator, int_1, int_2))

array.set(a_array, 33, f_calc_score(p_base / price_a34, trend_indicator, int_1, int_2))

array.set(a_array, 34, f_calc_score(p_base / price_a35, trend_indicator, int_1, int_2))

array.set(a_array, 35, f_calc_score(p_base / price_a36, trend_indicator, int_1, int_2))

array.set(a_array, 36, f_calc_score(p_base / price_a37, trend_indicator, int_1, int_2))

array.set(a_array, 37, f_calc_score(p_base / price_a38, trend_indicator, int_1, int_2))

array.set(a_array, 38, f_calc_score(p_base / price_a39, trend_indicator, int_1, int_2))

array.set(a_array, 39, f_calc_score(p_base / price_a40, trend_indicator, int_1, int_2))

a_array

Conditional Array Setting (f_arrayset):

This function checks if the number of used assets is greater than or equal to a specified number before populating the arrays.

// only set values into arrays for USED assets

f_arrayset(asset_number, a_array, p_base) =>

if (used_assets >= asset_number)

f_array_set(a_array, p_base)

else

na

Main Logic

The main logic initializes arrays to store scores for each asset. Each array corresponds to one asset's performance score.

Setting Trend Values: The code calls f_arrayset for each asset, populating the respective arrays with calculated scores based on the asset prices.

Combining Arrays: A combined_array is created to hold all the scores from individual asset arrays. This array facilitates further analysis, allowing for an overview of the performance scores of all assets at once.

// create a combined array (work-around since pinescript doesn't support having array of arrays)

var combined_array = array.new_int(40 * 40, 0)

if barstate.islast

for i = 0 to 39

array.set(combined_array, i, array.get(a1_array, i))

array.set(combined_array, i + (40 * 1), array.get(a2_array, i))

array.set(combined_array, i + (40 * 2), array.get(a3_array, i))

array.set(combined_array, i + (40 * 3), array.get(a4_array, i))

array.set(combined_array, i + (40 * 4), array.get(a5_array, i))

array.set(combined_array, i + (40 * 5), array.get(a6_array, i))

array.set(combined_array, i + (40 * 6), array.get(a7_array, i))

array.set(combined_array, i + (40 * 7), array.get(a8_array, i))

array.set(combined_array, i + (40 * 8), array.get(a9_array, i))

array.set(combined_array, i + (40 * 9), array.get(a10_array, i))

array.set(combined_array, i + (40 * 10), array.get(a11_array, i))

array.set(combined_array, i + (40 * 11), array.get(a12_array, i))

array.set(combined_array, i + (40 * 12), array.get(a13_array, i))

array.set(combined_array, i + (40 * 13), array.get(a14_array, i))

array.set(combined_array, i + (40 * 14), array.get(a15_array, i))

array.set(combined_array, i + (40 * 15), array.get(a16_array, i))

array.set(combined_array, i + (40 * 16), array.get(a17_array, i))

array.set(combined_array, i + (40 * 17), array.get(a18_array, i))

array.set(combined_array, i + (40 * 18), array.get(a19_array, i))

array.set(combined_array, i + (40 * 19), array.get(a20_array, i))

array.set(combined_array, i + (40 * 20), array.get(a21_array, i))

array.set(combined_array, i + (40 * 21), array.get(a22_array, i))

array.set(combined_array, i + (40 * 22), array.get(a23_array, i))

array.set(combined_array, i + (40 * 23), array.get(a24_array, i))

array.set(combined_array, i + (40 * 24), array.get(a25_array, i))

array.set(combined_array, i + (40 * 25), array.get(a26_array, i))

array.set(combined_array, i + (40 * 26), array.get(a27_array, i))

array.set(combined_array, i + (40 * 27), array.get(a28_array, i))

array.set(combined_array, i + (40 * 28), array.get(a29_array, i))

array.set(combined_array, i + (40 * 29), array.get(a30_array, i))

array.set(combined_array, i + (40 * 30), array.get(a31_array, i))

array.set(combined_array, i + (40 * 31), array.get(a32_array, i))

array.set(combined_array, i + (40 * 32), array.get(a33_array, i))

array.set(combined_array, i + (40 * 33), array.get(a34_array, i))

array.set(combined_array, i + (40 * 34), array.get(a35_array, i))

array.set(combined_array, i + (40 * 35), array.get(a36_array, i))

array.set(combined_array, i + (40 * 36), array.get(a37_array, i))

array.set(combined_array, i + (40 * 37), array.get(a38_array, i))

array.set(combined_array, i + (40 * 38), array.get(a39_array, i))

array.set(combined_array, i + (40 * 39), array.get(a40_array, i))

Calculating Sums: A separate array_sums is created to store the total score for each asset by summing the values of their respective score arrays. This allows for easy comparison of overall performance.

Ranking Assets: The final part of the code ranks the assets based on their total scores stored in array_sums. It assigns a rank to each asset, where the asset with the highest score receives the highest rank.

// create array for asset RANK based on array.sum

var ranks = array.new_int(used_assets, 0)

// for loop that calculates the rank of each asset

if barstate.islast

for i = 0 to (used_assets - 1)

int rank = 1

for x = 0 to (used_assets - 1)

if i != x

if array.get(array_sums, i) < array.get(array_sums, x)

rank := rank + 1

array.set(ranks, i, rank)

Dynamic Table Creation

Initialization: The table is initialized with a base structure that includes headers for asset names, scores, and ranks. The headers are set to remain constant, ensuring clarity for users as they interpret the displayed data.

Data Population: As scores are calculated for each asset, the corresponding values are dynamically inserted into the table. This is achieved through a loop that iterates over the scores and ranks stored in the combined_array and array_sums, respectively.

Automatic Extending Mechanism

Variable Asset Count: The code checks the number of assets defined by the user. Instead of hardcoding the number of rows in the table, it uses a variable to determine the extent of the data that needs to be displayed. This allows the table to expand or contract based on the number of assets being analyzed.

Dynamic Row Generation: Within the loop that populates the table, the code appends new rows for each asset based on the current asset count. The structure of each row includes the asset name, its score, and its rank, ensuring that the table remains consistent regardless of how many assets are involved.

// Automatically extending table based on the number of used assets

var table table = table.new(position.bottom_center, 50, 50, color.new(color.black, 100), color.white, 3, color.white, 1)

if barstate.islast

if not hide_head

table.cell(table, 0, 0, "Universal Ratio Trend Matrix", text_color = color.white, bgcolor = #010c3b, text_size = fontSize)

table.merge_cells(table, 0, 0, used_assets + 3, 0)

if not hide_inps

table.cell(table, 0, 1,

text = "Inputs: You are using " + str.tostring(trend_indicator) + ", which takes: " + str.tostring(f_get_input(trend_indicator)),

text_color = color.white, text_size = fontSize), table.merge_cells(table, 0, 1, used_assets + 3, 1)

table.cell(table, 0, 2, "Assets", text_color = color.white, text_size = fontSize, bgcolor = #010c3b)

for x = 0 to (used_assets - 1)

table.cell(table, x + 1, 2, text = str.tostring(array.get(assets, x)), text_color = color.white, bgcolor = #010c3b, text_size = fontSize)

table.cell(table, 0, x + 3, text = str.tostring(array.get(assets, x)), text_color = color.white, bgcolor = f_asset_col(array.get(ranks, x)), text_size = fontSize)

for r = 0 to (used_assets - 1)

for c = 0 to (used_assets - 1)

table.cell(table, c + 1, r + 3, text = str.tostring(array.get(combined_array, c + (r * 40))),

text_color = hl_type == "Text" ? f_get_col(array.get(combined_array, c + (r * 40))) : color.white, text_size = fontSize,

bgcolor = hl_type == "Background" ? f_get_col(array.get(combined_array, c + (r * 40))) : na)

for x = 0 to (used_assets - 1)

table.cell(table, x + 1, x + 3, "", bgcolor = #010c3b)

table.cell(table, used_assets + 1, 2, "", bgcolor = #010c3b)

for x = 0 to (used_assets - 1)

table.cell(table, used_assets + 1, x + 3, "==>", text_color = color.white)

table.cell(table, used_assets + 2, 2, "SUM", text_color = color.white, text_size = fontSize, bgcolor = #010c3b)

table.cell(table, used_assets + 3, 2, "RANK", text_color = color.white, text_size = fontSize, bgcolor = #010c3b)

for x = 0 to (used_assets - 1)

table.cell(table, used_assets + 2, x + 3,

text = str.tostring(array.get(array_sums, x)),

text_color = color.white, text_size = fontSize,

bgcolor = f_highlight_sum(array.get(array_sums, x), array.get(ranks, x)))

table.cell(table, used_assets + 3, x + 3,

text = str.tostring(array.get(ranks, x)),

text_color = color.white, text_size = fontSize,

bgcolor = f_highlight_rank(array.get(ranks, x)))

Markov Chain [3D] | FractalystWhat exactly is a Markov Chain?

This indicator uses a Markov Chain model to analyze, quantify, and visualize the transitions between market regimes (Bull, Bear, Neutral) on your chart. It dynamically detects these regimes in real-time, calculates transition probabilities, and displays them as animated 3D spheres and arrows, giving traders intuitive insight into current and future market conditions.

How does a Markov Chain work, and how should I read this spheres-and-arrows diagram?

Think of three weather modes: Sunny, Rainy, Cloudy.

Each sphere is one mode. The loop on a sphere means “stay the same next step” (e.g., Sunny again tomorrow).

The arrows leaving a sphere show where things usually go next if they change (e.g., Sunny moving to Cloudy).

Some paths matter more than others. A more prominent loop means the current mode tends to persist. A more prominent outgoing arrow means a change to that destination is the usual next step.

Direction isn’t symmetric: moving Sunny→Cloudy can behave differently than Cloudy→Sunny.

Now relabel the spheres to markets: Bull, Bear, Neutral.

Spheres: market regimes (uptrend, downtrend, range).

Self‑loop: tendency for the current regime to continue on the next bar.

Arrows: the most common next regime if a switch happens.

How to read: Start at the sphere that matches current bar state. If the loop stands out, expect continuation. If one outgoing path stands out, that switch is the typical next step. Opposite directions can differ (Bear→Neutral doesn’t have to match Neutral→Bear).

What states and transitions are shown?

The three market states visualized are:

Bullish (Bull): Upward or strong-market regime.

Bearish (Bear): Downward or weak-market regime.

Neutral: Sideways or range-bound regime.

Bidirectional animated arrows and probability labels show how likely the market is to move from one regime to another (e.g., Bull → Bear or Neutral → Bull).

How does the regime detection system work?

You can use either built-in price returns (based on adaptive Z-score normalization) or supply three custom indicators (such as volume, oscillators, etc.).

Values are statistically normalized (Z-scored) over a configurable lookback period.

The normalized outputs are classified into Bull, Bear, or Neutral zones.

If using three indicators, their regime signals are averaged and smoothed for robustness.

How are transition probabilities calculated?

On every confirmed bar, the algorithm tracks the sequence of detected market states, then builds a rolling window of transitions.

The code maintains a transition count matrix for all regime pairs (e.g., Bull → Bear).

Transition probabilities are extracted for each possible state change using Laplace smoothing for numerical stability, and frequently updated in real-time.

What is unique about the visualization?

3D animated spheres represent each regime and change visually when active.

Animated, bidirectional arrows reveal transition probabilities and allow you to see both dominant and less likely regime flows.

Particles (moving dots) animate along the arrows, enhancing the perception of regime flow direction and speed.

All elements dynamically update with each new price bar, providing a live market map in an intuitive, engaging format.

Can I use custom indicators for regime classification?

Yes! Enable the "Custom Indicators" switch and select any three chart series as inputs. These will be normalized and combined (each with equal weight), broadening the regime classification beyond just price-based movement.

What does the “Lookback Period” control?

Lookback Period (default: 100) sets how much historical data builds the probability matrix. Shorter periods adapt faster to regime changes but may be noisier. Longer periods are more stable but slower to adapt.

How is this different from a Hidden Markov Model (HMM)?

It sets the window for both regime detection and probability calculations. Lower values make the system more reactive, but potentially noisier. Higher values smooth estimates and make the system more robust.

How is this Markov Chain different from a Hidden Markov Model (HMM)?

Markov Chain (as here): All market regimes (Bull, Bear, Neutral) are directly observable on the chart. The transition matrix is built from actual detected regimes, keeping the model simple and interpretable.

Hidden Markov Model: The actual regimes are unobservable ("hidden") and must be inferred from market output or indicator "emissions" using statistical learning algorithms. HMMs are more complex, can capture more subtle structure, but are harder to visualize and require additional machine learning steps for training.

A standard Markov Chain models transitions between observable states using a simple transition matrix, while a Hidden Markov Model assumes the true states are hidden (latent) and must be inferred from observable “emissions” like price or volume data. In practical terms, a Markov Chain is transparent and easier to implement and interpret; an HMM is more expressive but requires statistical inference to estimate hidden states from data.

Markov Chain: states are observable; you directly count or estimate transition probabilities between visible states. This makes it simpler, faster, and easier to validate and tune.

HMM: states are hidden; you only observe emissions generated by those latent states. Learning involves machine learning/statistical algorithms (commonly Baum–Welch/EM for training and Viterbi for decoding) to infer both the transition dynamics and the most likely hidden state sequence from data.

How does the indicator avoid “repainting” or look-ahead bias?

All regime changes and matrix updates happen only on confirmed (closed) bars, so no future data is leaked, ensuring reliable real-time operation.

Are there practical tuning tips?

Tune the Lookback Period for your asset/timeframe: shorter for fast markets, longer for stability.

Use custom indicators if your asset has unique regime drivers.

Watch for rapid changes in transition probabilities as early warning of a possible regime shift.

Who is this indicator for?

Quants and quantitative researchers exploring probabilistic market modeling, especially those interested in regime-switching dynamics and Markov models.

Programmers and system developers who need a probabilistic regime filter for systematic and algorithmic backtesting:

The Markov Chain indicator is ideally suited for programmatic integration via its bias output (1 = Bull, 0 = Neutral, -1 = Bear).

Although the visualization is engaging, the core output is designed for automated, rules-based workflows—not for discretionary/manual trading decisions.

Developers can connect the indicator’s output directly to their Pine Script logic (using input.source()), allowing rapid and robust backtesting of regime-based strategies.

It acts as a plug-and-play regime filter: simply plug the bias output into your entry/exit logic, and you have a scientifically robust, probabilistically-derived signal for filtering, timing, position sizing, or risk regimes.

The MC's output is intentionally "trinary" (1/0/-1), focusing on clear regime states for unambiguous decision-making in code. If you require nuanced, multi-probability or soft-label state vectors, consider expanding the indicator or stacking it with a probability-weighted logic layer in your scripting.

Because it avoids subjectivity, this approach is optimal for systematic quants, algo developers building backtested, repeatable strategies based on probabilistic regime analysis.

What's the mathematical foundation behind this?

The mathematical foundation behind this Markov Chain indicator—and probabilistic regime detection in finance—draws from two principal models: the (standard) Markov Chain and the Hidden Markov Model (HMM).

How to use this indicator programmatically?

The Markov Chain indicator automatically exports a bias value (+1 for Bullish, -1 for Bearish, 0 for Neutral) as a plot visible in the Data Window. This allows you to integrate its regime signal into your own scripts and strategies for backtesting, automation, or live trading.

Step-by-Step Integration with Pine Script (input.source)

Add the Markov Chain indicator to your chart.

This must be done first, since your custom script will "pull" the bias signal from the indicator's plot.

In your strategy, create an input using input.source()

Example:

//@version=5

strategy("MC Bias Strategy Example")

mcBias = input.source(close, "MC Bias Source")

After saving, go to your script’s settings. For the “MC Bias Source” input, select the plot/output of the Markov Chain indicator (typically its bias plot).

Use the bias in your trading logic

Example (long only on Bull, flat otherwise):

if mcBias == 1

strategy.entry("Long", strategy.long)

else

strategy.close("Long")

For more advanced workflows, combine mcBias with additional filters or trailing stops.

How does this work behind-the-scenes?

TradingView’s input.source() lets you use any plot from another indicator as a real-time, “live” data feed in your own script (source).

The selected bias signal is available to your Pine code as a variable, enabling logical decisions based on regime (trend-following, mean-reversion, etc.).

This enables powerful strategy modularity : decouple regime detection from entry/exit logic, allowing fast experimentation without rewriting core signal code.

Integrating 45+ Indicators with Your Markov Chain — How & Why

The Enhanced Custom Indicators Export script exports a massive suite of over 45 technical indicators—ranging from classic momentum (RSI, MACD, Stochastic, etc.) to trend, volume, volatility, and oscillator tools—all pre-calculated, centered/scaled, and available as plots.

// Enhanced Custom Indicators Export - 45 Technical Indicators

// Comprehensive technical analysis suite for advanced market regime detection

//@version=6

indicator('Enhanced Custom Indicators Export | Fractalyst', shorttitle='Enhanced CI Export', overlay=false, scale=scale.right, max_labels_count=500, max_lines_count=500)

// |----- Input Parameters -----| //

momentum_group = "Momentum Indicators"

trend_group = "Trend Indicators"

volume_group = "Volume Indicators"

volatility_group = "Volatility Indicators"

oscillator_group = "Oscillator Indicators"

display_group = "Display Settings"

// Common lengths

length_14 = input.int(14, "Standard Length (14)", minval=1, maxval=100, group=momentum_group)

length_20 = input.int(20, "Medium Length (20)", minval=1, maxval=200, group=trend_group)

length_50 = input.int(50, "Long Length (50)", minval=1, maxval=200, group=trend_group)

// Display options

show_table = input.bool(true, "Show Values Table", group=display_group)

table_size = input.string("Small", "Table Size", options= , group=display_group)

// |----- MOMENTUM INDICATORS (15 indicators) -----| //

// 1. RSI (Relative Strength Index)

rsi_14 = ta.rsi(close, length_14)

rsi_centered = rsi_14 - 50

// 2. Stochastic Oscillator

stoch_k = ta.stoch(close, high, low, length_14)

stoch_d = ta.sma(stoch_k, 3)

stoch_centered = stoch_k - 50

// 3. Williams %R

williams_r = ta.stoch(close, high, low, length_14) - 100

// 4. MACD (Moving Average Convergence Divergence)

= ta.macd(close, 12, 26, 9)

// 5. Momentum (Rate of Change)

momentum = ta.mom(close, length_14)

momentum_pct = (momentum / close ) * 100

// 6. Rate of Change (ROC)

roc = ta.roc(close, length_14)

// 7. Commodity Channel Index (CCI)

cci = ta.cci(close, length_20)

// 8. Money Flow Index (MFI)

mfi = ta.mfi(close, length_14)

mfi_centered = mfi - 50

// 9. Awesome Oscillator (AO)

ao = ta.sma(hl2, 5) - ta.sma(hl2, 34)

// 10. Accelerator Oscillator (AC)

ac = ao - ta.sma(ao, 5)

// 11. Chande Momentum Oscillator (CMO)

cmo = ta.cmo(close, length_14)

// 12. Detrended Price Oscillator (DPO)

dpo = close - ta.sma(close, length_20)

// 13. Price Oscillator (PPO)

ppo = ta.sma(close, 12) - ta.sma(close, 26)

ppo_pct = (ppo / ta.sma(close, 26)) * 100

// 14. TRIX

trix_ema1 = ta.ema(close, length_14)

trix_ema2 = ta.ema(trix_ema1, length_14)

trix_ema3 = ta.ema(trix_ema2, length_14)

trix = ta.roc(trix_ema3, 1) * 10000

// 15. Klinger Oscillator

klinger = ta.ema(volume * (high + low + close) / 3, 34) - ta.ema(volume * (high + low + close) / 3, 55)

// 16. Fisher Transform

fisher_hl2 = 0.5 * (hl2 - ta.lowest(hl2, 10)) / (ta.highest(hl2, 10) - ta.lowest(hl2, 10)) - 0.25

fisher = 0.5 * math.log((1 + fisher_hl2) / (1 - fisher_hl2))

// 17. Stochastic RSI

stoch_rsi = ta.stoch(rsi_14, rsi_14, rsi_14, length_14)

stoch_rsi_centered = stoch_rsi - 50

// 18. Relative Vigor Index (RVI)

rvi_num = ta.swma(close - open)

rvi_den = ta.swma(high - low)

rvi = rvi_den != 0 ? rvi_num / rvi_den : 0

// 19. Balance of Power (BOP)

bop = (close - open) / (high - low)

// |----- TREND INDICATORS (10 indicators) -----| //

// 20. Simple Moving Average Momentum

sma_20 = ta.sma(close, length_20)

sma_momentum = ((close - sma_20) / sma_20) * 100

// 21. Exponential Moving Average Momentum

ema_20 = ta.ema(close, length_20)

ema_momentum = ((close - ema_20) / ema_20) * 100

// 22. Parabolic SAR

sar = ta.sar(0.02, 0.02, 0.2)

sar_trend = close > sar ? 1 : -1

// 23. Linear Regression Slope

lr_slope = ta.linreg(close, length_20, 0) - ta.linreg(close, length_20, 1)

// 24. Moving Average Convergence (MAC)

mac = ta.sma(close, 10) - ta.sma(close, 30)

// 25. Trend Intensity Index (TII)

tii_sum = 0.0

for i = 1 to length_20

tii_sum += close > close ? 1 : 0

tii = (tii_sum / length_20) * 100

// 26. Ichimoku Cloud Components

ichimoku_tenkan = (ta.highest(high, 9) + ta.lowest(low, 9)) / 2

ichimoku_kijun = (ta.highest(high, 26) + ta.lowest(low, 26)) / 2

ichimoku_signal = ichimoku_tenkan > ichimoku_kijun ? 1 : -1

// 27. MESA Adaptive Moving Average (MAMA)

mama_alpha = 2.0 / (length_20 + 1)

mama = ta.ema(close, length_20)

mama_momentum = ((close - mama) / mama) * 100

// 28. Zero Lag Exponential Moving Average (ZLEMA)

zlema_lag = math.round((length_20 - 1) / 2)

zlema_data = close + (close - close )

zlema = ta.ema(zlema_data, length_20)

zlema_momentum = ((close - zlema) / zlema) * 100

// |----- VOLUME INDICATORS (6 indicators) -----| //

// 29. On-Balance Volume (OBV)

obv = ta.obv

// 30. Volume Rate of Change (VROC)

vroc = ta.roc(volume, length_14)

// 31. Price Volume Trend (PVT)

pvt = ta.pvt

// 32. Negative Volume Index (NVI)

nvi = 0.0

nvi := volume < volume ? nvi + ((close - close ) / close ) * nvi : nvi

// 33. Positive Volume Index (PVI)

pvi = 0.0

pvi := volume > volume ? pvi + ((close - close ) / close ) * pvi : pvi

// 34. Volume Oscillator

vol_osc = ta.sma(volume, 5) - ta.sma(volume, 10)

// 35. Ease of Movement (EOM)

eom_distance = high - low

eom_box_height = volume / 1000000

eom = eom_box_height != 0 ? eom_distance / eom_box_height : 0

eom_sma = ta.sma(eom, length_14)

// 36. Force Index

force_index = volume * (close - close )

force_index_sma = ta.sma(force_index, length_14)

// |----- VOLATILITY INDICATORS (10 indicators) -----| //

// 37. Average True Range (ATR)

atr = ta.atr(length_14)

atr_pct = (atr / close) * 100

// 38. Bollinger Bands Position

bb_basis = ta.sma(close, length_20)

bb_dev = 2.0 * ta.stdev(close, length_20)

bb_upper = bb_basis + bb_dev

bb_lower = bb_basis - bb_dev

bb_position = bb_dev != 0 ? (close - bb_basis) / bb_dev : 0

bb_width = bb_dev != 0 ? (bb_upper - bb_lower) / bb_basis * 100 : 0

// 39. Keltner Channels Position

kc_basis = ta.ema(close, length_20)

kc_range = ta.ema(ta.tr, length_20)

kc_upper = kc_basis + (2.0 * kc_range)

kc_lower = kc_basis - (2.0 * kc_range)

kc_position = kc_range != 0 ? (close - kc_basis) / kc_range : 0

// 40. Donchian Channels Position

dc_upper = ta.highest(high, length_20)

dc_lower = ta.lowest(low, length_20)

dc_basis = (dc_upper + dc_lower) / 2

dc_position = (dc_upper - dc_lower) != 0 ? (close - dc_basis) / (dc_upper - dc_lower) : 0

// 41. Standard Deviation

std_dev = ta.stdev(close, length_20)

std_dev_pct = (std_dev / close) * 100

// 42. Relative Volatility Index (RVI)

rvi_up = ta.stdev(close > close ? close : 0, length_14)

rvi_down = ta.stdev(close < close ? close : 0, length_14)

rvi_total = rvi_up + rvi_down

rvi_volatility = rvi_total != 0 ? (rvi_up / rvi_total) * 100 : 50

// 43. Historical Volatility

hv_returns = math.log(close / close )

hv = ta.stdev(hv_returns, length_20) * math.sqrt(252) * 100

// 44. Garman-Klass Volatility

gk_vol = math.log(high/low) * math.log(high/low) - (2*math.log(2)-1) * math.log(close/open) * math.log(close/open)

gk_volatility = math.sqrt(ta.sma(gk_vol, length_20)) * 100

// 45. Parkinson Volatility

park_vol = math.log(high/low) * math.log(high/low)

parkinson = math.sqrt(ta.sma(park_vol, length_20) / (4 * math.log(2))) * 100

// 46. Rogers-Satchell Volatility

rs_vol = math.log(high/close) * math.log(high/open) + math.log(low/close) * math.log(low/open)

rogers_satchell = math.sqrt(ta.sma(rs_vol, length_20)) * 100

// |----- OSCILLATOR INDICATORS (5 indicators) -----| //

// 47. Elder Ray Index

elder_bull = high - ta.ema(close, 13)

elder_bear = low - ta.ema(close, 13)

elder_power = elder_bull + elder_bear

// 48. Schaff Trend Cycle (STC)

stc_macd = ta.ema(close, 23) - ta.ema(close, 50)

stc_k = ta.stoch(stc_macd, stc_macd, stc_macd, 10)

stc_d = ta.ema(stc_k, 3)

stc = ta.stoch(stc_d, stc_d, stc_d, 10)

// 49. Coppock Curve

coppock_roc1 = ta.roc(close, 14)

coppock_roc2 = ta.roc(close, 11)

coppock = ta.wma(coppock_roc1 + coppock_roc2, 10)

// 50. Know Sure Thing (KST)

kst_roc1 = ta.roc(close, 10)

kst_roc2 = ta.roc(close, 15)

kst_roc3 = ta.roc(close, 20)

kst_roc4 = ta.roc(close, 30)

kst = ta.sma(kst_roc1, 10) + 2*ta.sma(kst_roc2, 10) + 3*ta.sma(kst_roc3, 10) + 4*ta.sma(kst_roc4, 15)

// 51. Percentage Price Oscillator (PPO)

ppo_line = ((ta.ema(close, 12) - ta.ema(close, 26)) / ta.ema(close, 26)) * 100

ppo_signal = ta.ema(ppo_line, 9)

ppo_histogram = ppo_line - ppo_signal

// |----- PLOT MAIN INDICATORS -----| //

// Plot key momentum indicators

plot(rsi_centered, title="01_RSI_Centered", color=color.purple, linewidth=1)

plot(stoch_centered, title="02_Stoch_Centered", color=color.blue, linewidth=1)

plot(williams_r, title="03_Williams_R", color=color.red, linewidth=1)

plot(macd_histogram, title="04_MACD_Histogram", color=color.orange, linewidth=1)

plot(cci, title="05_CCI", color=color.green, linewidth=1)

// Plot trend indicators

plot(sma_momentum, title="06_SMA_Momentum", color=color.navy, linewidth=1)

plot(ema_momentum, title="07_EMA_Momentum", color=color.maroon, linewidth=1)

plot(sar_trend, title="08_SAR_Trend", color=color.teal, linewidth=1)

plot(lr_slope, title="09_LR_Slope", color=color.lime, linewidth=1)

plot(mac, title="10_MAC", color=color.fuchsia, linewidth=1)

// Plot volatility indicators

plot(atr_pct, title="11_ATR_Pct", color=color.yellow, linewidth=1)

plot(bb_position, title="12_BB_Position", color=color.aqua, linewidth=1)

plot(kc_position, title="13_KC_Position", color=color.olive, linewidth=1)

plot(std_dev_pct, title="14_StdDev_Pct", color=color.silver, linewidth=1)

plot(bb_width, title="15_BB_Width", color=color.gray, linewidth=1)

// Plot volume indicators

plot(vroc, title="16_VROC", color=color.blue, linewidth=1)

plot(eom_sma, title="17_EOM", color=color.red, linewidth=1)

plot(vol_osc, title="18_Vol_Osc", color=color.green, linewidth=1)

plot(force_index_sma, title="19_Force_Index", color=color.orange, linewidth=1)

plot(obv, title="20_OBV", color=color.purple, linewidth=1)

// Plot additional oscillators

plot(ao, title="21_Awesome_Osc", color=color.navy, linewidth=1)

plot(cmo, title="22_CMO", color=color.maroon, linewidth=1)

plot(dpo, title="23_DPO", color=color.teal, linewidth=1)

plot(trix, title="24_TRIX", color=color.lime, linewidth=1)

plot(fisher, title="25_Fisher", color=color.fuchsia, linewidth=1)

// Plot more momentum indicators

plot(mfi_centered, title="26_MFI_Centered", color=color.yellow, linewidth=1)

plot(ac, title="27_AC", color=color.aqua, linewidth=1)

plot(ppo_pct, title="28_PPO_Pct", color=color.olive, linewidth=1)

plot(stoch_rsi_centered, title="29_StochRSI_Centered", color=color.silver, linewidth=1)

plot(klinger, title="30_Klinger", color=color.gray, linewidth=1)

// Plot trend continuation

plot(tii, title="31_TII", color=color.blue, linewidth=1)

plot(ichimoku_signal, title="32_Ichimoku_Signal", color=color.red, linewidth=1)

plot(mama_momentum, title="33_MAMA_Momentum", color=color.green, linewidth=1)

plot(zlema_momentum, title="34_ZLEMA_Momentum", color=color.orange, linewidth=1)

plot(bop, title="35_BOP", color=color.purple, linewidth=1)

// Plot volume continuation

plot(nvi, title="36_NVI", color=color.navy, linewidth=1)

plot(pvi, title="37_PVI", color=color.maroon, linewidth=1)

plot(momentum_pct, title="38_Momentum_Pct", color=color.teal, linewidth=1)

plot(roc, title="39_ROC", color=color.lime, linewidth=1)

plot(rvi, title="40_RVI", color=color.fuchsia, linewidth=1)

// Plot volatility continuation

plot(dc_position, title="41_DC_Position", color=color.yellow, linewidth=1)

plot(rvi_volatility, title="42_RVI_Volatility", color=color.aqua, linewidth=1)

plot(hv, title="43_Historical_Vol", color=color.olive, linewidth=1)

plot(gk_volatility, title="44_GK_Volatility", color=color.silver, linewidth=1)

plot(parkinson, title="45_Parkinson_Vol", color=color.gray, linewidth=1)

// Plot final oscillators

plot(rogers_satchell, title="46_RS_Volatility", color=color.blue, linewidth=1)

plot(elder_power, title="47_Elder_Power", color=color.red, linewidth=1)

plot(stc, title="48_STC", color=color.green, linewidth=1)

plot(coppock, title="49_Coppock", color=color.orange, linewidth=1)

plot(kst, title="50_KST", color=color.purple, linewidth=1)

// Plot final indicators

plot(ppo_histogram, title="51_PPO_Histogram", color=color.navy, linewidth=1)

plot(pvt, title="52_PVT", color=color.maroon, linewidth=1)

// |----- Reference Lines -----| //

hline(0, "Zero Line", color=color.gray, linestyle=hline.style_dashed, linewidth=1)

hline(50, "Midline", color=color.gray, linestyle=hline.style_dotted, linewidth=1)

hline(-50, "Lower Midline", color=color.gray, linestyle=hline.style_dotted, linewidth=1)

hline(25, "Upper Threshold", color=color.gray, linestyle=hline.style_dotted, linewidth=1)

hline(-25, "Lower Threshold", color=color.gray, linestyle=hline.style_dotted, linewidth=1)

// |----- Enhanced Information Table -----| //

if show_table and barstate.islast

table_position = position.top_right

table_text_size = table_size == "Tiny" ? size.tiny : table_size == "Small" ? size.small : size.normal

var table info_table = table.new(table_position, 3, 18, bgcolor=color.new(color.white, 85), border_width=1, border_color=color.gray)

// Headers

table.cell(info_table, 0, 0, 'Category', text_color=color.black, text_size=table_text_size, bgcolor=color.new(color.blue, 70))

table.cell(info_table, 1, 0, 'Indicator', text_color=color.black, text_size=table_text_size, bgcolor=color.new(color.blue, 70))

table.cell(info_table, 2, 0, 'Value', text_color=color.black, text_size=table_text_size, bgcolor=color.new(color.blue, 70))

// Key Momentum Indicators

table.cell(info_table, 0, 1, 'MOMENTUM', text_color=color.purple, text_size=table_text_size, bgcolor=color.new(color.purple, 90))

table.cell(info_table, 1, 1, 'RSI Centered', text_color=color.purple, text_size=table_text_size)

table.cell(info_table, 2, 1, str.tostring(rsi_centered, '0.00'), text_color=color.purple, text_size=table_text_size)

table.cell(info_table, 0, 2, '', text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 1, 2, 'Stoch Centered', text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 2, 2, str.tostring(stoch_centered, '0.00'), text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 0, 3, '', text_color=color.red, text_size=table_text_size)

table.cell(info_table, 1, 3, 'Williams %R', text_color=color.red, text_size=table_text_size)

table.cell(info_table, 2, 3, str.tostring(williams_r, '0.00'), text_color=color.red, text_size=table_text_size)

table.cell(info_table, 0, 4, '', text_color=color.orange, text_size=table_text_size)

table.cell(info_table, 1, 4, 'MACD Histogram', text_color=color.orange, text_size=table_text_size)

table.cell(info_table, 2, 4, str.tostring(macd_histogram, '0.000'), text_color=color.orange, text_size=table_text_size)

table.cell(info_table, 0, 5, '', text_color=color.green, text_size=table_text_size)

table.cell(info_table, 1, 5, 'CCI', text_color=color.green, text_size=table_text_size)

table.cell(info_table, 2, 5, str.tostring(cci, '0.00'), text_color=color.green, text_size=table_text_size)

// Key Trend Indicators

table.cell(info_table, 0, 6, 'TREND', text_color=color.navy, text_size=table_text_size, bgcolor=color.new(color.navy, 90))

table.cell(info_table, 1, 6, 'SMA Momentum %', text_color=color.navy, text_size=table_text_size)

table.cell(info_table, 2, 6, str.tostring(sma_momentum, '0.00'), text_color=color.navy, text_size=table_text_size)

table.cell(info_table, 0, 7, '', text_color=color.maroon, text_size=table_text_size)

table.cell(info_table, 1, 7, 'EMA Momentum %', text_color=color.maroon, text_size=table_text_size)

table.cell(info_table, 2, 7, str.tostring(ema_momentum, '0.00'), text_color=color.maroon, text_size=table_text_size)

table.cell(info_table, 0, 8, '', text_color=color.teal, text_size=table_text_size)

table.cell(info_table, 1, 8, 'SAR Trend', text_color=color.teal, text_size=table_text_size)

table.cell(info_table, 2, 8, str.tostring(sar_trend, '0'), text_color=color.teal, text_size=table_text_size)

table.cell(info_table, 0, 9, '', text_color=color.lime, text_size=table_text_size)

table.cell(info_table, 1, 9, 'Linear Regression', text_color=color.lime, text_size=table_text_size)

table.cell(info_table, 2, 9, str.tostring(lr_slope, '0.000'), text_color=color.lime, text_size=table_text_size)

// Key Volatility Indicators

table.cell(info_table, 0, 10, 'VOLATILITY', text_color=color.yellow, text_size=table_text_size, bgcolor=color.new(color.yellow, 90))

table.cell(info_table, 1, 10, 'ATR %', text_color=color.yellow, text_size=table_text_size)

table.cell(info_table, 2, 10, str.tostring(atr_pct, '0.00'), text_color=color.yellow, text_size=table_text_size)

table.cell(info_table, 0, 11, '', text_color=color.aqua, text_size=table_text_size)

table.cell(info_table, 1, 11, 'BB Position', text_color=color.aqua, text_size=table_text_size)

table.cell(info_table, 2, 11, str.tostring(bb_position, '0.00'), text_color=color.aqua, text_size=table_text_size)

table.cell(info_table, 0, 12, '', text_color=color.olive, text_size=table_text_size)

table.cell(info_table, 1, 12, 'KC Position', text_color=color.olive, text_size=table_text_size)

table.cell(info_table, 2, 12, str.tostring(kc_position, '0.00'), text_color=color.olive, text_size=table_text_size)

// Key Volume Indicators

table.cell(info_table, 0, 13, 'VOLUME', text_color=color.blue, text_size=table_text_size, bgcolor=color.new(color.blue, 90))

table.cell(info_table, 1, 13, 'Volume ROC', text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 2, 13, str.tostring(vroc, '0.00'), text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 0, 14, '', text_color=color.red, text_size=table_text_size)

table.cell(info_table, 1, 14, 'EOM', text_color=color.red, text_size=table_text_size)

table.cell(info_table, 2, 14, str.tostring(eom_sma, '0.000'), text_color=color.red, text_size=table_text_size)

// Key Oscillators

table.cell(info_table, 0, 15, 'OSCILLATORS', text_color=color.purple, text_size=table_text_size, bgcolor=color.new(color.purple, 90))

table.cell(info_table, 1, 15, 'Awesome Osc', text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 2, 15, str.tostring(ao, '0.000'), text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 0, 16, '', text_color=color.red, text_size=table_text_size)

table.cell(info_table, 1, 16, 'Fisher Transform', text_color=color.red, text_size=table_text_size)

table.cell(info_table, 2, 16, str.tostring(fisher, '0.000'), text_color=color.red, text_size=table_text_size)

// Summary Statistics

table.cell(info_table, 0, 17, 'SUMMARY', text_color=color.black, text_size=table_text_size, bgcolor=color.new(color.gray, 70))

table.cell(info_table, 1, 17, 'Total Indicators: 52', text_color=color.black, text_size=table_text_size)

regime_color = rsi_centered > 10 ? color.green : rsi_centered < -10 ? color.red : color.gray

regime_text = rsi_centered > 10 ? "BULLISH" : rsi_centered < -10 ? "BEARISH" : "NEUTRAL"

table.cell(info_table, 2, 17, regime_text, text_color=regime_color, text_size=table_text_size)

This makes it the perfect “indicator backbone” for quantitative and systematic traders who want to prototype, combine, and test new regime detection models—especially in combination with the Markov Chain indicator.

How to use this script with the Markov Chain for research and backtesting:

Add the Enhanced Indicator Export to your chart.

Every calculated indicator is available as an individual data stream.

Connect the indicator(s) you want as custom input(s) to the Markov Chain’s “Custom Indicators” option.

In the Markov Chain indicator’s settings, turn ON the custom indicator mode.

For each of the three custom indicator inputs, select the exported plot from the Enhanced Export script—the menu lists all 45+ signals by name.

This creates a powerful, modular regime-detection engine where you can mix-and-match momentum, trend, volume, or custom combinations for advanced filtering.

Backtest regime logic directly.

Once you’ve connected your chosen indicators, the Markov Chain script performs regime detection (Bull/Neutral/Bear) based on your selected features—not just price returns.

The regime detection is robust, automatically normalized (using Z-score), and outputs bias (1, -1, 0) for plug-and-play integration.

Export the regime bias for programmatic use.

As described above, use input.source() in your Pine Script strategy or system and link the bias output.

You can now filter signals, control trade direction/size, or design pairs-trading that respect true, indicator-driven market regimes.

With this framework, you’re not limited to static or simplistic regime filters. You can rigorously define, test, and refine what “market regime” means for your strategies—using the technical features that matter most to you.

Optimize your signal generation by backtesting across a universe of meaningful indicator blends.

Enhance risk management with objective, real-time regime boundaries.

Accelerate your research: iterate quickly, swap indicator components, and see results with minimal code changes.

Automate multi-asset or pairs-trading by integrating regime context directly into strategy logic.

Add both scripts to your chart, connect your preferred features, and start investigating your best regime-based trades—entirely within the TradingView ecosystem.

References & Further Reading

Ang, A., & Bekaert, G. (2002). “Regime Switches in Interest Rates.” Journal of Business & Economic Statistics, 20(2), 163–182.

Hamilton, J. D. (1989). “A New Approach to the Economic Analysis of Nonstationary Time Series and the Business Cycle.” Econometrica, 57(2), 357–384.

Markov, A. A. (1906). "Extension of the Limit Theorems of Probability Theory to a Sum of Variables Connected in a Chain." The Notes of the Imperial Academy of Sciences of St. Petersburg.

Guidolin, M., & Timmermann, A. (2007). “Asset Allocation under Multivariate Regime Switching.” Journal of Economic Dynamics and Control, 31(11), 3503–3544.

Murphy, J. J. (1999). Technical Analysis of the Financial Markets. New York Institute of Finance.

Brock, W., Lakonishok, J., & LeBaron, B. (1992). “Simple Technical Trading Rules and the Stochastic Properties of Stock Returns.” Journal of Finance, 47(5), 1731–1764.

Zucchini, W., MacDonald, I. L., & Langrock, R. (2017). Hidden Markov Models for Time Series: An Introduction Using R (2nd ed.). Chapman and Hall/CRC.

On Quantitative Finance and Markov Models:

Lo, A. W., & Hasanhodzic, J. (2009). The Heretics of Finance: Conversations with Leading Practitioners of Technical Analysis. Bloomberg Press.

Patterson, S. (2016). The Man Who Solved the Market: How Jim Simons Launched the Quant Revolution. Penguin Press.

TradingView Pine Script Documentation: www.tradingview.com

TradingView Blog: “Use an Input From Another Indicator With Your Strategy” www.tradingview.com

GeeksforGeeks: “What is the Difference Between Markov Chains and Hidden Markov Models?” www.geeksforgeeks.org

What makes this indicator original and unique?

- On‑chart, real‑time Markov. The chain is drawn directly on your chart. You see the current regime, its tendency to stay (self‑loop), and the usual next step (arrows) as bars confirm.

- Source‑agnostic by design. The engine runs on any series you select via input.source() — price, your own oscillator, a composite score, anything you compute in the script.

- Automatic normalization + regime mapping. Different inputs live on different scales. The script standardizes your chosen source and maps it into clear regimes (e.g., Bull / Bear / Neutral) without you micromanaging thresholds each time.

- Rolling, bar‑by‑bar learning. Transition tendencies are computed from a rolling window of confirmed bars. What you see is exactly what the market did in that window.

- Fast experimentation. Switch the source, adjust the window, and the Markov view updates instantly. It’s a rapid way to test ideas and feel regime persistence/switch behavior.

Integrate your own signals (using input.source())

- In settings, choose the Source . This is powered by input.source() .

- Feed it price, an indicator you compute inside the script, or a custom composite series.

- The script will automatically normalize that series and process it through the Markov engine, mapping it to regimes and updating the on‑chart spheres/arrows in real time.

Credits:

Deep gratitude to @RicardoSantos for both the foundational Markov chain processing engine and inspiring open-source contributions, which made advanced probabilistic market modeling accessible to the TradingView community.

Special thanks to @Alien_Algorithms for the innovative and visually stunning 3D sphere logic that powers the indicator’s animated, regime-based visualization.

Disclaimer

This tool summarizes recent behavior. It is not financial advice and not a guarantee of future results.

DTC AIO [India] v2.0DTC AIO v2.0 – Advanced Technical Analysis Suite

This indicator is a comprehensive dashboard designed specifically for Indian equities, providing traders with a unique blend of trend, volatility, volume, and earnings analytics—all in one panel.

Key Features

Multi-Timeframe Volatility Tables:

Instantly view daily, weekly, and monthly Average Daily Range (ADR) values in a compact, color-coded table.

Relative Volume (RVol) Panel:

Displays real-time relative volume in crores, helping you spot unusual activity at a glance.

Strength Gauge:

A proprietary scoring system that quantifies the frequency and magnitude of price bursts, giving you a unique “Strength” score for each symbol.

Earnings & Sales Table:

Automatically fetches and displays quarterly EPS and sales data, with YoY and QoQ growth, color-coded for clarity.

Theme-Aware Design:

All tables and overlays adapt to dark or light chart themes for maximum readability.

Customizable Watermark:

Add your own signature, timeframe, and price change watermark to the chart, with full control over position and color.